Four Capitals, Four Readings:

How the May 7 Tariff Ruling Lands in Beijing, Mexico City, Brussels, and Ottawa

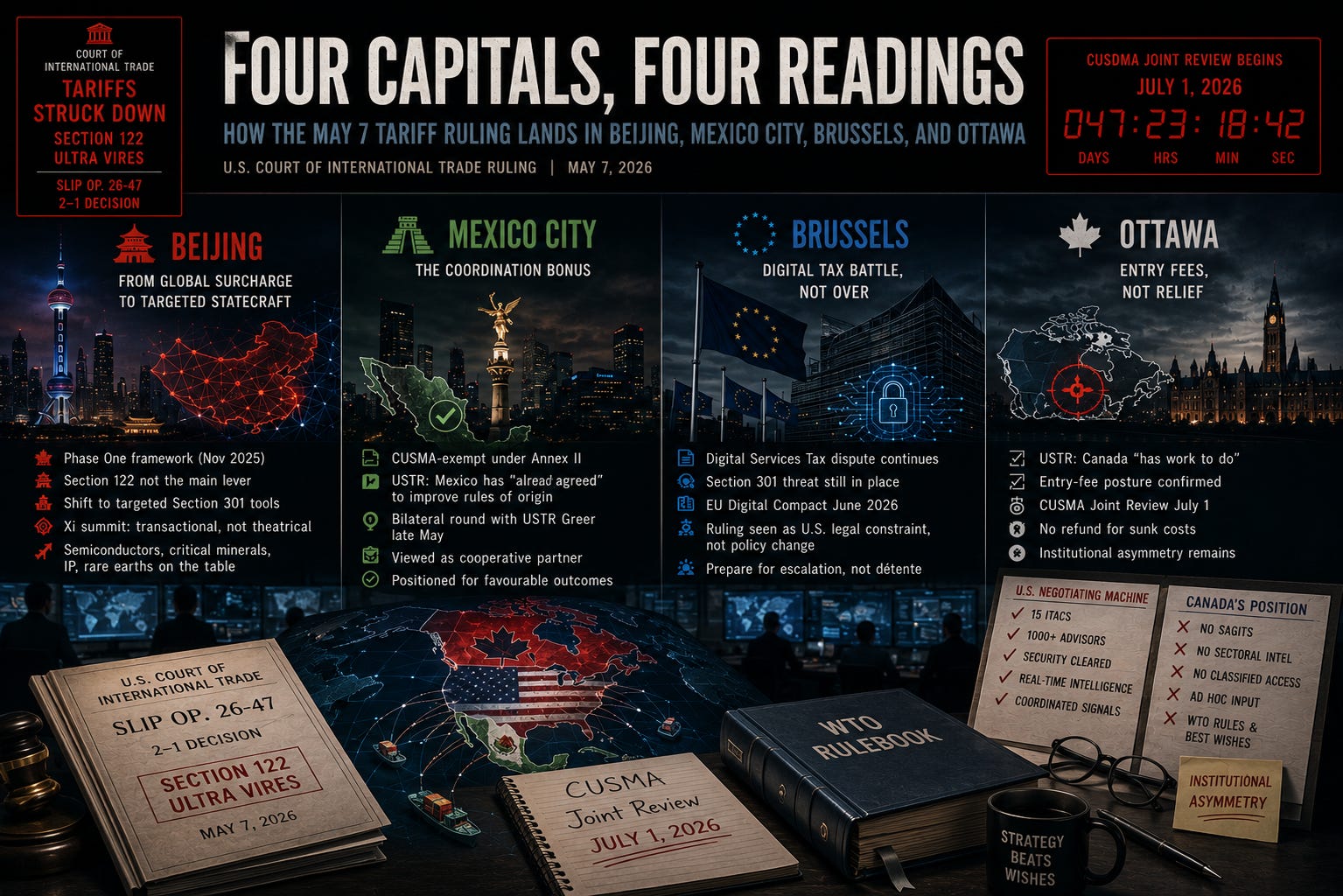

The Court of International Trade has struck down President Trump’s 10% global surcharge. The decision arrives in different rooms in different ways. In none of them does it reduce the United States’ underlying leverage. It clarifies which instruments the administration will use next.

On May 7, 2026, by a 2-1 vote, the United States Court of International Trade struck down President Trump’s 10% global Section 122 tariff. The decision is technical, narrow, and divided. It runs eighty-eight pages and is published as Slip Op. 26-47.1

The substantive holding is straightforward. Section 122 of the Trade Act of 1974 requires “balance-of-payments deficits” measured by the methods Congress understood in 1974, not by current-account or trade-deficit data. The President’s February 20 Proclamation pointed to the wrong concept and was therefore ultra vires. A permanent injunction was issued for the State of Washington and two private importers. The remaining twenty-three plaintiff states were dismissed without prejudice for lack of Article III standing. The administration has sixty days to appeal to the Federal Circuit and almost certainly will.2

The ruling reads differently in different capitals. Beijing reads it through the lens of the Phase One framework signed in November 2025 and the upcoming Trump-Xi summit. Mexico City reads it through the lens of the bilateral CUSMA round opening with USTR Greer in late May. Brussels reads it through the lens of the digital services tax dispute that has structured trans-Atlantic trade tension for half a decade. Ottawa reads it through the lens of an entry-fee posture the administration has confirmed in the Joint Review run-up.

In each capital, the conclusion is the same: this ruling does not reduce the United States’ leverage. It reshapes how that leverage will be deployed. This is a strategic-level walk through what each reading looks like.

I. Beijing: From Global Surcharge to Targeted Statecraft

The Section 122 ruling lands one week before the scheduled Trump-Xi summit. That timing matters more than the substance of the ruling itself.

China’s exposure to the Section 122 surcharge was indirect. China was not exempt from the 10 percent rate, but the rate stacked on top of an existing layer of Section 301 tariffs that already governed the bilateral commercial relationship. The November 2025 framework between the United States and China suspended the Section 301 maritime, logistics, and shipbuilding tariffs that had been imposed earlier in 2025. The December 2025 Section 301 determination on China’s targeting of the semiconductor industry remains in force, but the implementing tariffs have been calibrated rather than fully deployed. The Section 122 layer was real. It was not the operative architecture.

What the May 7 ruling does is shift the United States’ negotiating posture from the global surcharge instrument to the targeted Section 301 architecture. Beijing reads this as a structural pivot, not as a relief.

The administration’s preferred posture against China is sectoral. The semiconductor finding, the maritime and shipbuilding finding, and the pending Section 232 investigations on critical minerals are all instruments that operate against China specifically through targeted commercial mechanisms. They are also instruments the administration controls more directly than the global tariff architecture. The May 7 ruling does not touch any of them.

For the Xi summit, this means a less theatrical and more transactional negotiation. Sweeping commercial resets are unlikely. Phased Section 301 relief in exchange for specific Chinese commitments on semiconductor cooperation, critical minerals processing, rare earth export licensing, and intellectual property treatment is the architecture being pursued. The administration enters the summit with diminished global tariff leverage but with sharpened targeted-instrument leverage. From Beijing’s vantage, the deck is shorter but the cards still in play are sharper.

The November 2025 National Security Strategy framed China as the long-term strategic competitor whose containment requires “American economic and technological preeminence.”3 Section 232 and Section 301 are the instruments through which that containment is operationalized. Section 122 was not. Beijing has been preparing for the targeted environment all along. The May 7 ruling confirms which environment now applies.

II. Mexico City: The Coordination Bonus

Mexico’s exposure to the Section 122 surcharge was zero. Mexican goods qualifying under CUSMA were exempted under Annex II of the Proclamation, alongside Canadian goods and goods from six Central American and Caribbean parties. The ruling, in narrow terms, removes an exemption Mexico did not need.

In broader terms, the ruling arrives in a particular moment in the bilateral United States-Mexico relationship. On April 20, 2026, USTR Greer met Mexican President Claudia Sheinbaum in advance of the first formal United States-Mexico bilateral CUSMA negotiating round, scheduled for late May.4 In testimony to the House Ways and Means Committee on April 22, USTR Greer praised Mexico explicitly. Mexico had “already agreed” to improve CUSMA rules of origin, while Canada had not.5 The administration is publicly differentiating the two CUSMA partners.

For Mexico City, the Section 122 ruling arrives as confirmation of a strategy the Sheinbaum government has been pursuing since the start of 2026: structured engagement, demonstrated cooperation, and explicit signaling on the issues the United States has identified as priority concerns. That strategy was not contingent on Section 122. It was always about the post-Section 122 environment. The Section 232 investigation on automotive imports, the rules-of-origin updates the administration is demanding, and the labour-enforcement architecture under CUSMA Chapter 23 are the operative instruments. Mexico’s positioning around all three has been positive enough to produce the formal bilateral round announcement.

The May 7 ruling reinforces Mexico’s strategic position. It does not require a new approach. The administration has now lost the global-surcharge lever, but it retains the sectoral and country-specific levers around which Mexico has already been engaging.

The wider implication is that the United States now has greater incentive to differentiate Mexico from Canada in the Joint Review. The Section 122 ruling has eroded the administration’s ability to apply uniform pressure across the CUSMA partners. The administration’s response, predictably, is to apply differentiated pressure. Mexico is being rewarded for cooperation. Canada is being signaled, in increasingly explicit terms, that it has not yet earned the same treatment.

III. Brussels: The DST Fault Line

For Europe, the Section 122 ruling reads as a sideshow to the main fight. The main fight is over digital services taxes.

The administration has been clear since the start of 2025 that it views European DSTs as discriminatory measures targeting United States technology companies. On April 22, 2026, USTR Greer testified that Section 301 actions against DSTs had been drafted and stand ready for use. He noted that the United States had reached agreements with nine other countries prohibiting digital service taxes. He confirmed he would meet EU Trade Commissioner Maroš Šefčovič the following Friday to discuss DSTs among other topics. He noted that the French government had recently shelved plans to raise its digital service tax, but that French officials at the EU Council of Member States have advocated for a bloc-wide DST targeting United States firms.6

The Section 122 ruling does not address any of this. It does not constrain Section 301. It does not touch digital services or technology policy. The ruling is, from Brussels’ vantage, technical in a domain that does not bear on the operative dispute.

What the ruling does do is alter the trans-Atlantic balance in a subtle way. The Section 122 surcharge was a horizontal instrument that hit European exports across the board. Its removal eases a European cost burden that Brussels had been preparing to challenge through WTO consultations and counter-tariff threats. That easing reduces the operational cost of the trans-Atlantic trade dispute on Europe’s side and removes one rationale for European retaliatory escalation.

In exchange, Europe now faces an administration that has been told by the Court of International Trade that its preferred horizontal instrument is unavailable, and which must therefore concentrate its energies on the targeted instruments. Section 301 actions against European DSTs are the administration’s most likely instrument of escalation. Brussels has prepared for those actions. What it had not necessarily prepared for is the timing acceleration that the May 7 ruling creates. The administration, having lost its horizontal lever, has institutional incentive to deploy its sectoral and targeted levers faster.

The trans-Atlantic outlook for the second half of 2026 is therefore a sharper Section 301 dispute on Digital Sales Taxes and a deeper conversation on technology standards and digital trade architecture. The 10 percent surcharge is gone. The DST fight is amplified. Brussels is, on net, no better off than it was on May 6, and possibly worse.

IV. Ottawa: The Most Exposed Reading

Of the four capitals, Ottawa reads the May 7 ruling with the highest stakes.

Canada was the principal beneficiary of the discarded Section 122 exemption. Canada faces an administration that has been publicly differentiating it from Mexico, that has drafted Section 301 actions on digital services taxes, that has initiated its first Section 301 investigation in the modern era against Canadian labour practices, and that has conditioned formal Joint Review talks on upfront Canadian concessions described by sources as an “entry fee” covering dairy quota administration, digital sovereignty policy, and provincial alcohol bans.7

For Ottawa, the ruling is not a relief. It is a recalibration of risk. The Canadian shelter was specific to Section 122. It does not extend to Section 232. It does not extend to Section 301. It does not extend to Section 338. It does not extend to the IEEPA non-tariff toolkit the President has separately claimed.

What Ottawa now faces is a multi-instrument environment in which the administration’s leverage has shifted from a global surcharge that exempted Canada to a constellation of sectoral and country-specific instruments that do not. The Joint Review, opening July 1, 2026, will be the principal venue for resolving how that leverage is deployed.

The Canadian situation is sufficiently distinct from the others to require its own treatment. I will publish that analysis as a companion piece in this series.8 The high-level point for the global frame is this: of the four capitals reading the May 7 ruling, Ottawa is the one whose situation has changed most. The exemption that protected Canadian goods is gone. The instruments that target Canadian technology, innovation, and regulatory policy remain in full force. The Joint Review will be the venue at which the Administration tests how much of its technology-dominance agenda Canada is prepared to absorb.

V. The Common Thread

The four readings share a common feature. In none of them does the May 7 ruling reduce the underlying United States leverage.

Beijing trades a removed surcharge for sharpened targeted instruments. Mexico City finds its existing strategy reinforced. Brussels exchanges horizontal pressure for accelerated DST enforcement. Ottawa loses a country-specific shelter without acquiring any equivalent protection in the wider toolkit.

The underlying logic is that the May 7 ruling addresses the legal authority for one tariff instrument. It does not address the underlying United States posture, which treats trade authority as a broader instrument of economic statecraft. The administration’s own reading of the February 20 Supreme Court decision in Learning Resources, Inc. v. Trump makes the posture explicit:

“the Supreme Court’s decision today made a President’s ability to both regulate Trade, and impose TARIFFS, more powerful and crystal clear, rather than less... the Supreme Court did not overrule TARIFFS, they merely overruled a particular use of IEEPA TARIFFS... a President can actually charge more TARIFFS than I was charging in the past under the various other TARIFF authorities, which have also been confirmed, and fully allowed.” 9

That posture has not changed on May 7. The administration’s reaction to the May 7 ruling, voiced by President Trump that evening, was that “we always do it a different way. We get one ruling and we do it a different way.” 10 That is the operating instruction. The operative architecture is being shifted from horizontal to targeted, from global to sectoral, from one instrument to a portfolio.

The four capitals read this differently because they face different combinations of those instruments. None of them reads it as the United States retreating.

What the May 7 ruling has done is force a single answer to a strategic question that had previously been deferred: which instruments will the administration use to advance its trade and technology agenda over the second half of 2026? The horizontal surcharge is no longer one of them. Section 232, Section 301, Section 338, and the IEEPA non-tariff toolkit all are. The instruments still in play are sharper, more targeted, and harder to defend against than the instrument the courts have removed.

The deck has been shuffled. The dealer still holds it, and the advantage goes to the house. The cards now visible are the cards that always mattered most.

Prof. Barry Appleton is Co-Director and Distinguished Senior Fellow at the Center for International Law at New York Law School, Interim Director of the Balsillie Legal Advisory Centre at the Balsillie School of International Affairs and Managing Partner of Appleton & Associates International Lawyers LP. His Substack, Appleton’s Clause & Effect, addresses trade architecture and economic sovereignty.

State of Oregon v. Trump, Slip Op. 26-47 (Ct. Int’l Trade, May 7, 2026), available at https://www.cit.uscourts.gov/sites/cit/files/26-47.pdf.

A government appeal must be filed within 60 days under Federal Rule of Appellate Procedure 4(a)(1)(B). The Section 122 statutory authority sunsets July 24, 2026 regardless of the appeal. The administration is expected to seek a stay of the injunction pending appeal under FRAP 8.

The White House, National Security Strategy of the United States of America (Nov. 2025).

Bloomberg News, Greer-Sheinbaum Meeting Sets Stage for May U.S.-Mexico CUSMA Round (Apr. 20, 2026).

Hearing on the President’s Trade Policy Agenda Before the H. Comm. on Ways and Means, 119th Cong. (Apr. 22, 2026) (testimony of Jamieson Greer, U.S. Trade Representative).

Dylan Moroses, USTR Seeking ‘Outcomes’ on DSTs, Stronger USMCA Rules, Law360 (Apr. 22, 2026).

CBC News and Radio-Canada, Washington Demanding ‘Entry Fee’ from Ottawa Before Trade Talks: Sources (Apr. 22, 2026).

See “Canada After the Shuffle: The May 7 Tariff Ruling, the Technology Dominance Agenda, and the Joint Review Risk Map,” Clause and Effect (forthcoming).

Statement by President Donald J. Trump on the Supreme Court Decision in Learning Resources, Inc. v. Trump (Feb. 20, 2026).

President Trump, remarks to reporters, evening of May 7, 2026, as reported in Bloomberg News